Tax Briefs

Click here to go back

Five tax implications of divorce

Are you in the early stages of divorce? In addition to the tough personal issues that you’re dealing with, several tax concerns need to be addressed to ensure that taxes are kept to a minimum and that important tax-related decisions are properly made. Here are five issues to consider if you’re in the process of getting a divorce.

- Alimony or support payments. For alimony under divorce or separation agreements that are executed after 2018, there’s no deduction for alimony and separation support payments for the spouse making them. And the alimony payments aren’t included in the gross income of the spouse receiving them. (The rules are different for divorce or separation agreements executed before 2019.)

- Child support. No matter when the divorce or separation instrument is executed, child support payments aren’t deductible by the paying spouse (or taxable to the recipient).

- Personal residence. In general, if a married couple sells their home in connection with a divorce or legal separation, they should be able to avoid tax on up to $500,000 of gain (as long as they’ve owned and used the residence as their principal residence for two of the previous five years). If one spouse continues to live in the home and the other moves out (but they both remain owners of the home), they may still be able to avoid gain on the future sale of the home (up to $250,000 each), but special language may have to be included in the divorce decree or separation agreement to protect this tax exclusion for the spouse who moves out.

If the couple doesn’t meet the two-year ownership and use tests, any gain from the sale may qualify for a reduced exclusion due to unforeseen circumstances. - Pension benefits. A spouse’s pension benefits are often part of a divorce property settlement. In these cases, the commonly preferred method to handle the benefits is to get a “qualified domestic relations order” (QDRO). This gives one spouse the right to share in the pension benefits of the other and taxes the spouse who receives the benefits. Without a QDRO the spouse who earned the benefits will still be taxed on them even though they’re paid out to the other spouse.

- Business interests. If certain types of business interests are transferred in connection with divorce, care should be taken to make sure “tax attributes” aren’t forfeited. For example, interests in S corporations may result in “suspended” losses (losses that are carried into future years instead of being deducted in the year they’re incurred). When these interests change hands in a divorce, the suspended losses may be forfeited. If a partnership interest is transferred, a variety of more complex issues may arise involving partners’ shares of partnership debt, capital accounts, built-in gains on contributed property, and other complex issues.

A variety of other issues

These are just some of the issues you may have to deal with if you’re getting a divorce. In addition, you must decide how to file your tax return (single, married filing jointly, married filing separately or head of household). You may need to adjust your income tax withholding and you should notify the IRS of any new address or name change. There are also estate planning considerations. We can help you work through all of the financial issues involved in divorce.

Businesses will soon be able to deduct more under the standard mileage rate

Business owners are aware that the price of gas is historically high, which has made their vehicle costs soar. The average nationwide price of a gallon of unleaded regular gas on June 17 was $5, compared with $3.08 a year earlier, according to the AAA Gas Prices website. A gallon of diesel averaged $5.78 a gallon, compared with $3.21 a year earlier.

Fortunately, the IRS is providing some relief. The tax agency announced an increase in the optional standard mileage rate for the last six months of 2022. Taxpayers may use the optional cents-per-mile rate to calculate the deductible costs of operating a vehicle for business.

For the second half of 2022 (July 1–December 31), the standard mileage rate for business travel will be 62.5 cents per mile, up from 58.5 cents per mile for the first half of the year (January 1–June 30). There are different standard mileage rates for charitable and medical driving.

Special situation

Raising the standard mileage rate in the middle of the year is unusual. Normally, the IRS updates the mileage rates once a year at the end of the year for the next calendar year. However, the tax agency explained that “in recognition of recent gasoline price increases, the IRS made this special adjustment for the final months of 2022.” But while the move is uncommon, it’s not without precedent. The standard mileage rate was increased for the last six months of 2011 and 2008 after gas prices rose significantly.

While fuel costs are a significant factor in the mileage figure, the IRS notes that “other items enter into the calculation of mileage rates, such as depreciation and insurance and other fixed and variable costs.”

Two options

The optional standard mileage rate is one of two methods a business can use to compute the deductible costs of operating an automobile for business puroses. Taxpayers also have the option of calculating the actual costs of using their vehicles rather than using the standard mileage rate. This may include expenses such as gas, oil, tires, insurance, repairs, licenses, vehicle registration fees and a depreciation allowance for the vehicle.

From a tax standpoint, you may get a larger deduction by tracking the actual expense method than you would with the standard mileage rate. But many taxpayers don’t want to spend time tracking actual costs. Be aware that there are rules that may prevent you from using one method or the other. For example, if a business wants to use the standard mileage rate for a car it leases, the business must use this rate for the entire lease period. Consult with us about your particular circumstances to determine the best course of action.

Simple ways to make strategic planning a reality

Every business wants to engage in strategic planning that will better position the company to sell more to current customers — and perhaps expand into new markets. Yet the term “strategic planning” is so broad. It’s easy to get overwhelmed by all the possible directions you could go in and have a hard time choosing a path. Here are a few simple ways to make strategic planning a reality.

Focus on who you already know

One cost-effective strategy is to work more closely with current customers by strengthening and expanding those relationships. After all, they’re presumably satisfied with the products or services you’re currently offering, so they’re likely willing to try others. Ask about their needs, listen to their responses and look for ways to better serve them and boost revenue.

Another strategy is to partner with other compatible businesses, perhaps locally or in your industry. You might not be able to produce certain complementary products or services, but you could team up with another company that can and, together, both businesses could see their bottom lines grow.

Dig deeper into social media

By now, most companies have dipped their respective and figurative toes into social media. These online platforms can be a cost-effective way to highlight specific products or services, as well as to familiarize the buying public with your brand and culture. Of course, you’ve got to handle social media promotions carefully — customers tend to be turned off by a barrage of posts that basically shout, “Buy this!”

Nonetheless, digging deeper into the use and analytics of social media can play a viable role in a broader strategic plan. Many experts recommend alternating posts that focus on specific products or services with those providing helpful, informative content to followers. For example, a cybersecurity firm might offer tips on staying safe online.

Reevaluate your pricing strategy

Although increasing prices might boost revenue if sales remain steady, scattershot price jumps can prompt customers to go elsewhere. That’s why a critical component to any strategic plan must be designing a pricing strategy that boosts revenue without simply slapping on a higher price tag.

One option is bundling products or services and then offering the bundle at a lower price than what customers would pay in total for each item individually. Customers enjoy the savings while the company boosts sales, often with minimal additional effort.

Another way might be to offer a subscription service. Customers get uninterrupted access to the products or services they need, and the business establishes an ongoing revenue source.

Don’t hesitate

A good strategic plan first addresses broad objectives and then narrows down to specific steps. The next time you and your leadership team get stuck, don’t hesitate to back up and look at some big picture issues. Let us assist you in assessing the profitability impact of any of the strategic planning ideas you come up with.

Caring for an elderly relative? You may be eligible for tax breaks

Taking care of an elderly parent or grandparent may provide more than just personal satisfaction. You could also be eligible for tax breaks. Here’s a rundown of some of them.

1. Medical expenses. If the individual qualifies as your “medical dependent,” and you itemize deductions on your tax return, you can include any medical expenses you incur for the individual along with your own when determining your medical deduction. The test for determining whether an individual qualifies as your “medical dependent” is less stringent than that used to determine whether an individual is your “dependent,” which is discussed below. In general, an individual qualifies as a medical dependent if you provide over 50% of his or her support, including medical costs.

However, bear in mind that medical expenses are deductible only to the extent they exceed 7.5% of your adjusted gross income (AGI).

The costs of qualified long-term care services required by a chronically ill individual and eligible long-term care insurance premiums are included in the definition of deductible medical expenses. There’s an annual cap on the amount of premiums that can be deducted. The cap is based on age, going as high as $5,640 for 2022 for an individual over 70.

2. Filing status. If you aren’t married, you may qualify for “head of household” status by virtue of the individual you’re caring for. You can claim this status if:

- The person you’re caring for lives in your household,

- You cover more than half the household costs,

- The person qualifies as your “dependent,” and

- The person is a relative.

If the person you’re caring for is your parent, the person doesn’t need to live with you, so long as you provide more than half of the person’s household costs and the person qualifies as your dependent. A head of household has a higher standard deduction and lower tax rates than a single filer.

3. Tests for determining whether your loved one is a “dependent.” Dependency exemptions are suspended (or disallowed) for 2018–2025. Even though the dependency exemption is currently suspended, the dependency tests still apply when it comes to determining whether a taxpayer is entitled to various other tax benefits, such as head-of-household filing status.

For an individual to qualify as your “dependent,” the following must be true for the tax year at issue:

- You must provide more than 50% of the individual’s support costs,

- The individual must either live with you or be related,

- The individual must not have gross income in excess of an inflation-adjusted exemption amount,

- The individual can’t file a joint return for the year, and

- The individual must be a U.S. citizen or a resident of the U.S., Canada or Mexico.

4. Dependent care credit. If the cared-for individual qualifies as your dependent, lives with you, and physically or mentally can’t take care of him- or herself, you may qualify for the dependent care credit for costs you incur for the individual’s care to enable you and your spouse to go to work.

Contact us if you’d like to further discuss the tax aspects of financially supporting and caring for an elderly relative.

Valuable gifts to charity may require an appraisal

If you donate valuable items to charity, you may be required to get an appraisal. The IRS requires donors and charitable organizations to supply certain information to prove their right to deduct charitable contributions. If you donate an item of property (or a group of similar items) worth more than $5,000, certain appraisal requirements apply. You must:

- Get a “qualified appraisal,”

- Receive the qualified appraisal before your tax return is due,

- Attach an “appraisal summary” to the first tax return on which the deduction is claimed,

- Include other information with the return, and

- Maintain certain records.

Keep these definitions in mind. A qualified appraisal is a complex and detailed document. It must be prepared and signed by a qualified appraiser. An appraisal summary is a summary of a qualified appraisal made on Form 8283 and attached to the donor’s return.

While courts have allowed taxpayers some latitude in meeting the “qualified appraisal” rules, you should aim for exact compliance.

The qualified appraisal isn’t submitted separately to the IRS in most cases. Instead, the appraisal summary, which is a separate statement prepared on an IRS form, is attached to the donor’s tax return. However, a copy of the appraisal must be attached for gifts of art valued at $20,000 or more and for all gifts of property valued at more than $500,000, other than inventory, publicly traded stock and intellectual property. If an item has been appraised at $50,000 or more, you can ask the IRS to issue a “Statement of Value” that can be used to substantiate the value.

Failure to comply with the requirements

The penalty for failing to get a qualified appraisal and attach an appraisal summary to the return is denial of the charitable deduction. The deduction may be lost even if the property was valued correctly. There may be relief if the failure was due to reasonable cause.

Exceptions to the requirement

A qualified appraisal isn’t required for contributions of:

- A car, boat or airplane for which the deduction is limited to the charity’s gross sales proceeds,

- stock in trade, inventory or property held primarily for sale to customers in the ordinary course of business,

- publicly traded securities for which market quotations are “readily available,” and

- qualified intellectual property, such as a patent.

Also, only a partially completed appraisal summary must be attached to the tax return for contributions of:

- Nonpublicly traded stock for which the claimed deduction is greater than $5,000 and doesn’t exceed $10,000, and

- Publicly traded securities for which market quotations aren’t “readily available.”

More than one gift

If you make gifts of two or more items during a tax year, even to multiple charitable organizations, the claimed values of all property of the same category or type (such as stamps, paintings, books, stock that isn’t publicly traded, land, jewelry, furniture or toys) are added together in determining whether the $5,000 or $10,000 limits are exceeded.

The bottom line is you must be careful to comply with the appraisal requirements or risk disallowance of your charitable deduction. Contact us if you have any further questions or want to discuss your contribution planning.

The tax mechanics involved in the sale of trade or business property

What are the tax consequences of selling property used in your trade or business?

There are many rules that can potentially apply to the sale of business property. Thus, to simplify discussion, let’s assume that the property you want to sell is land or depreciable property used in your business, and has been held by you for more than a year. (There are different rules for property held primarily for sale to customers in the ordinary course of business; intellectual property; low-income housing; property that involves farming or livestock; and other types of property.)

General rules

Under the Internal Revenue Code, your gains and losses from sales of business property are netted against each other. The net gain or loss qualifies for tax treatment as follows:

1) If the netting of gains and losses results in a net gain, then long-term capital gain treatment results, subject to “recapture” rules discussed below. Long-term capital gain treatment is generally more favorable than ordinary income treatment.

2) If the netting of gains and losses results in a net loss, that loss is fully deductible against ordinary income (in other words, none of the rules that limit the deductibility of capital losses apply).

Recapture rules

The availability of long-term capital gain treatment for business property net gain is limited by “recapture” rules — that is, rules under which amounts are treated as ordinary income rather than capital gain because of previous ordinary loss or deduction treatment for these amounts.

There’s a special recapture rule that applies only to business property. Under this rule, to the extent you’ve had a business property net loss within the previous five years, any business property net gain is treated as ordinary income instead of as long-term capital gain.

Section 1245 Property

“Section 1245 Property” consists of all depreciable personal property, whether tangible or intangible, and certain depreciable real property (usually, real property that performs specific functions). If you sell Section 1245 Property, you must recapture your gain as ordinary income to the extent of your earlier depreciation deductions on the asset.

Section 1250 Property

“Section 1250 Property” consists, generally, of buildings and their structural components. If you sell Section 1250 Property that was placed in service after 1986, none of the long-term capital gain attributable to depreciation deductions will be subject to depreciation recapture. However, for most noncorporate taxpayers, the gain attributable to depreciation deductions, to the extent it doesn’t exceed business property net gain, will (as reduced by the business property recapture rule above) be taxed at a rate of no more than 28.8% (25% as adjusted for the 3.8% net investment income tax) rather than the maximum 23.8% rate (20% as adjusted for the 3.8% net investment income tax) that generally applies to long-term capital gains of noncorporate taxpayers.

Other rules may apply to Section 1250 Property, depending on when it was placed in service.

As you can see, even with the simplifying assumptions in this article, the tax treatment of the sale of business assets can be complex. Contact us if you’d like to determine the tax consequences of specific transactions or if you have any additional questions.

Want to turn a hobby into a business? Watch out for the tax rules

Like many people, you may have dreamed of turning a hobby into a regular business. You won’t have any tax headaches if your new business is profitable. But what if the new enterprise consistently generates losses (your deductions exceed income) and you claim them on your tax return? You can generally deduct losses for expenses incurred in a bona fide business. However, the IRS may step in and say the venture is a hobby — an activity not engaged in for profit — rather than a business. Then you’ll be unable to deduct losses.

By contrast, if the new enterprise isn’t affected by the hobby loss rules because it’s profitable, all otherwise allowable expenses are deductible on Schedule C, even if they exceed income from the enterprise.

Note: Before 2018, deductible hobby expenses had to be claimed as miscellaneous itemized deductions subject to a 2%-of-AGI “floor.” However, because miscellaneous deductions aren’t allowed from 2018 through 2025, deductible hobby expenses are effectively wiped out from 2018 through 2025.

Avoiding a hobby designation

There are two ways to avoid the hobby loss rules:

- Show a profit in at least three out of five consecutive years (two out of seven years for breeding, training, showing or racing horses).

- Run the venture in such a way as to show that you intend to turn it into a profit-maker, rather than operate it as a mere hobby. The IRS regs themselves say that the hobby loss rules won’t apply if the facts and circumstances show that you have a profit-making objective.

How can you prove you have a profit-making objective? You should run the venture in a businesslike manner. The IRS and the courts will look at the following factors:

- How you run the activity,

- Your expertise in the area (and your advisors’ expertise),

- The time and effort you expend in the enterprise,

- Whether there’s an expectation that the assets used in the activity will rise in value,

- Your success in carrying on other activities,

- Your history of income or loss in the activity,

- The amount of any occasional profits earned,

- Your financial status, and

- Whether the activity involves elements of personal pleasure or recreation.

Recent court case

In one U.S. Tax Court case, a married couple’s miniature donkey breeding activity was found to be conducted with a profit motive. The IRS had earlier determined it was a hobby and the couple was liable for taxes and penalties for the two tax years in which they claimed losses of more than $130,000. However, the court found the couple had a business plan, kept separate records and conducted the activity in a businesslike manner. The court stated they were “engaged in the breeding activity with an actual and honest objective of making a profit.” (TC Memo 2021-140)

Contact us for more details on whether a venture of yours may be affected by the hobby loss rules, and what you should do to avoid a tax challenge.

Businesses looking for outside investors need a sturdy pitch deck

Is your business ready to seek funding from outside investors? Perhaps you’re a start-up that needs money to launch as robustly as possible. Or maybe your company has been operating for a while and you want to pivot in a new direction or just take it to the next level.

Whatever the case may be, seeking outside investment isn’t as cut and dried as applying for a commercial loan. You need to wow investors with your vision, financials and business plan.

To do so, many businesses today put together a “pitch deck.” This is a digital presentation that provides a succinct, compelling description of the company, its solution to a market need, and the benefits of the investment opportunity. Here are some useful guidelines:

Keep it brief, between 10 to 12 short slides. You want to make a positive impression and whet investors’ interest without taking up too much of their time. You can follow up with additional details later.

Be concise but comprehensive. State your company’s mission (why it exists), vision (where it wants to go) and value proposition (what your product or service does for customers). Also declare upfront how much money you’d like to raise.

Identify the problem you’re solving. Explain the gap in the market that you’re addressing. Discuss it realistically and with minimal jargon, so investors can quickly grasp the challenge and intuitively agree with you.

Describe your target market. Include the market’s size, composition and forecasted growth. Resist the temptation to define the market as “everyone,” because this tends to come across as unrealistic.

Outline your business plan. That is, how will your business make money? What will you charge customers for your solution? Are you a premium provider or is this a budget-minded product or service?

Summarize your marketing and sales plans. Describe the marketing tactics you’ll employ to garner attention and interact with your customer base. Then identify your optimal sales channels and methods. If you already have a strong social media following, note that as well.

Sell your leadership team. Who are you and your fellow owners/executives? What are your educational and business backgrounds? Perhaps above everything else, investors will demand that a trustworthy crew is steering the ship.

Provide a snapshot of your financials, both past and future. But don’t just copy and paste your financial statements onto a few slides. Use aesthetically pleasing charts, graphs and other visuals to show historical results (if available), as well as forecasted sales and income for the next several years. Your profit projections should realistically flow from historical performance or at least appear feasible given expected economic and market conditions.

Identify your competitors. What other companies are addressing the problem that your product or service solves? Differentiate yourself from those businesses and explain why customers will choose your solution over theirs.

Describe how you’ll use the funds. Show investors how their investment will allow you to fulfill your stated business objectives. Be as specific as possible about where the money will go.

Ask for help. As you undertake the steps above — and before you meet with investors — contact our firm. We can help you develop a pitch deck with accurate, pertinent financial data that will capture investors’ interest and help you get the funding your business needs.

Thinking about converting your home into a rental property?

In some cases, homeowners decide to move to new residences, but keep their present homes and rent them out. If you’re thinking of doing this, you’re probably aware of the financial risks and rewards. However, you also should know that renting out your home carries potential tax benefits and pitfalls.

You’re generally treated as a regular real estate landlord once you begin renting your home. That means you must report rental income on your tax return, but also are entitled to offsetting landlord deductions for the money you spend on utilities, operating expenses, incidental repairs and maintenance (for example, fixing a leak in the roof). Additionally, you can claim depreciation deductions for the home. You can fully offset rental income with otherwise allowable landlord deductions.

Passive activity rules

However, under the passive activity loss (PAL) rules, you may not be able to currently claim the rent-related deductions that exceed your rental income unless an exception applies. Under the most widely applicable exception, the PAL rules won’t affect your converted property for a tax year in which your adjusted gross income doesn’t exceed $100,000, you actively participate in running the home-rental business, and your losses from all rental real estate activities in which you actively participate don’t exceed $25,000.

You should also be aware that potential tax pitfalls may arise from renting your residence. Unless your rentals are strictly temporary and are made necessary by adverse market conditions, you could forfeit an important tax break for home sellers if you finally sell the home at a profit. In general, you can escape tax on up to $250,000 ($500,000 for married couples filing jointly) of gain on the sale of your principal home. However, this tax-free treatment is conditioned on your having used the residence as your principal residence for at least two of the five years preceding the sale. So renting your home out for an extended time could jeopardize a big tax break.

Even if you don’t rent out your home so long as to jeopardize your principal residence exclusion, the tax break you would have gotten on the sale (the $250,000/$500,000 exclusion) won’t apply to the extent of any depreciation allowable with respect to the rental or business use of the home for periods after May 6, 1997, or to any gain allocable to a period of nonqualified use (any period during which the property isn’t used as the principal residence of the taxpayer or the taxpayer’s spouse or former spouse) after December 31, 2008. A maximum tax rate of 25% will apply to this gain (attributable to depreciation deductions).

Selling at a loss

Some homeowners who bought at the height of a market may ultimately sell at a loss someday. In such situations, the loss is available for tax purposes only if the owner can establish that the home was in fact converted permanently into income-producing property. Here, a longer lease period helps an owner. However, if you’re in this situation, be aware that you may not wind up with much of a loss for tax purposes. That’s because basis (the cost for tax purposes) is equal to the lesser of actual cost or the property’s fair market value when it’s converted to rental property. So if a home was bought for $300,000, converted to a rental when it’s worth $250,000, and ultimately sold for $225,000, the loss would be only $25,000.

The question of whether to turn a principal residence into rental property isn’t easy. Contact us to review your situation and help you make a decision.

Tax considerations when adding a new partner at your business

Adding a new partner in a partnership has several financial and legal implications. Let’s say you and your partners are planning to admit a new partner. The new partner will acquire a one-third interest in the partnership by making a cash contribution to it. Let’s further assume that your bases in your partnership interests are sufficient so that the decrease in your portions of the partnership’s liabilities because of the new partner’s entry won’t reduce your bases to zero.

Not as simple as it seems

Although the entry of a new partner appears to be a simple matter, it’s necessary to plan the new person’s entry properly in order to avoid various tax problems. Here are two issues to consider:

First, if there’s a change in the partners’ interests in unrealized receivables and substantially appreciated inventory items, the change is treated as a sale of those items, with the result that the current partners will recognize gain. For this purpose, unrealized receivables include not only accounts receivable, but also depreciation recapture and certain other ordinary income items. In order to avoid gain recognition on those items, it’s necessary that they be allocated to the current partners even after the entry of the new partner.

Second, the tax code requires that the “built-in gain or loss” on assets that were held by the partnership before the new partner was admitted be allocated to the current partners and not to the entering partner. Generally speaking, “built-in gain or loss” is the difference between the fair market value and basis of the partnership property at the time the new partner is admitted.

The most important effect of these rules is that the new partner must be allocated a portion of the depreciation equal to his share of the depreciable property based on current fair market value. This will reduce the amount of depreciation that can be taken by the current partners. The other effect is that the built-in gain or loss on the partnership assets must be allocated to the current partners when partnership assets are sold. The rules that apply here are complex and the partnership may have to adopt special accounting procedures to cope with the relevant requirements.

Keep track of your basis

When adding a partner or making other changes, a partner’s basis in his or her interest can undergo frequent adjustment. It’s imperative to keep proper track of your basis because it can have an impact in several areas: gain or loss on the sale of your interest, how partnership distributions to you are taxed and the maximum amount of partnership loss you can deduct.

Contact us if you’d like help in dealing with these issues or any other issues that may arise in connection with your partnership.

Offering summer job opportunities? Double-check child labor laws

Spring has sprung — and summer isn’t far off. If your business typically hires minors for summer jobs, now’s a good time to brush up on child labor laws.

In News Release No. 22-546-DEN, the U.S. Department of Labor’s Wage and Hour Division (WHD) recently announced that it’s stepping up efforts to identify child labor violations in the Salt Lake City area. However, the news serves as a good reminder to companies nationwide about the many details of employing children.

Finer points of the FLSA

The Department of Labor is the sole federal agency that monitors child labor and enforces child labor laws. The most sweeping federal law that restricts the employment and abuse of child workers is the Fair Labor Standards Act (FLSA). The WHD handles enforcement of the FLSA’s child labor provisions.

The FLSA restricts the hours that children under 16 years of age can work and lists hazardous occupations too dangerous for young workers to perform. Examples include jobs involving the operation of power-driven woodworking machines, and work that involves exposure to radioactive substances and ionizing radiators.

The FLSA allows children 14 to 15 years old to work outside of school hours in various manufacturing, non-mining, non-hazardous jobs under certain conditions. Permissible work hours for 14- and 15-year-olds are:

- Three hours on a school day,

- 18 hours in a school week,

- Eight hours on a non-school day,

- 40 hours in a non-school week, and

- Between 7 a.m. and 7 p.m.*

*From June 1 through Labor Day, nighttime work hours are extended to 9 p.m.

Just one example

News Release No. 22-546-DEN reveals the results of three specific investigations. In them, the WHD found that employers had allowed minors to operate dangerous machinery. Also, minors were allowed to work beyond the time permitted, during school hours, more than three hours on a school night and more than 18 hours a workweek.

In one case, a restaurant allowed minors to operate or assist in operating a trash compactor and a manual fryer, which are prohibited tasks for 14- and 15-year-old workers. The employer also allowed minors to work:

- More than three hours on a school day,

- More than 18 hours in a school week,

- Past 7 p.m. from Labor Day through May 31,

- Past 9 p.m. from June 1 through Labor Day, and

- More than eight hours on a non-school day.

The WHD assessed the business $17,159 in civil money penalties.

Letter of the law

In the news release, WHD Director Kevin Hunt states, “Early employment opportunities are meant to be valuable and safe learning experiences for young people and should never put them at risk of harm. Employers who fail to keep minor-aged workers safe and follow child labor regulations may struggle to find the young people they need to operate their businesses.”

What’s more, as the case above demonstrates, companies can incur substantial financial penalties for failing to follow the letter of the law. Consult an employment attorney for further details on the FLSA. We can help you measure and manage your hiring and payroll costs.

Once you file your tax return, consider these 3 issues

The tax filing deadline for 2021 tax returns is April 18 this year. After your 2021 tax return has been successfully filed with the IRS, there may still be some issues to bear in mind. Here are three considerations:

1. You can throw some tax records away now

You should hang onto tax records related to your return for as long as the IRS can audit your return or assess additional taxes. The statute of limitations is generally three years after you file your return. So you can generally get rid of most records related to tax returns for 2018 and earlier years. (If you filed an extension for your 2018 return, hold on to your records until at least three years from when you filed the extended return.)

However, the statute of limitations extends to six years for taxpayers who understate their gross income by more than 25%.

You should keep certain tax-related records longer. For example, keep the actual tax returns indefinitely, so you can prove to the IRS that you filed a legitimate return. (There’s no statute of limitations for an audit if you didn’t file a return or you filed a fraudulent one.)

What about your retirement account paperwork? Keep records associated with a retirement account until you’ve depleted the account and reported the last withdrawal on your tax return, plus three (or six) years. And retain records related to real estate or investments for as long as you own the asset, plus at least three years after you sell it and report the sale on your tax return. (You can keep these records for six years if you want to be extra safe.)

2. Waiting for your refund? You can check on it

The IRS has an online tool that can tell you the status of your refund. Go to irs.gov and click on “Get Your Refund Status” to find out about yours. You’ll need your Social Security number, filing status and the exact refund amount.

3. If you forgot to report something, you can file an amended return

In general, you can file an amended tax return and claim a refund within three years after the date you filed your original return or within two years of the date you paid the tax, whichever is later. So for a 2021 tax return that you file on April 15, 2022, you can generally file an amended return until April 15, 2025.

However, there are a few opportunities when you have longer to file an amended return. For example, the statute of limitations for bad debts is longer than the usual three-year time limit for most items on your tax return. In general, you can amend your tax return to claim a bad debt for seven years from the due date of the tax return for the year that the debt became worthless.

We’re here year round

If you have questions about tax record retention, your refund or filing an amended return, contact us. We’re not just available at tax filing time — we’re here all year!

Tax issues to assess when converting from a C corporation to an S corporation

Operating as an S corporation may help reduce federal employment taxes for small businesses in the right circumstances. Although S corporations may provide tax advantages over C corporations, there are some potentially costly tax issues that you should assess before making a decision to switch.

Here’s a quick rundown of the most important issues to consider when converting from a C corporation to an S corporation:

Built-in gains tax

Although S corporations generally aren’t subject to tax, those that were formerly C corporations are taxed on built-in gains (such as appreciated property) that the C corporation has when the S election becomes effective, if those gains are recognized within 5 years after the corporation becomes an S corporation. This is generally unfavorable, although there are situations where the S election still can produce a better tax result despite the built-in gains tax.

Passive income

S corporations that were formerly C corporations are subject to a special tax if their passive investment income (such as dividends, interest, rents, royalties and stock sale gains) exceeds 25% of their gross receipts, and the S corporation has accumulated earnings and profits carried over from its C corporation years. If that tax is owed for three consecutive years, the corporation’s election to be an S corporation terminates. You can avoid the tax by distributing the accumulated earnings and profits, which would be taxable to shareholders. Or you might want to avoid the tax by limiting the amount of passive income.

LIFO inventories

C corporations that use LIFO inventories have to pay tax on the benefits they derived by using LIFO if they convert to S corporations. The tax can be spread over four years. This cost must be weighed against the potential tax gains from converting to S status.

Unused losses

If your C corporation has unused net operating losses, the losses can't be used to offset its income as an S corporation and can’t be passed through to shareholders. If the losses can’t be carried back to an earlier C corporation year, it will be necessary to weigh the cost of giving up the losses against the tax savings expected to be generated by the switch to S status.

There are other factors to consider in switching from C to S status. Shareholder-employees of S corporations can’t get the full range of tax-free fringe benefits that are available with a C corporation. And there may be complications for shareholders who have outstanding loans from their qualified plans. All of these factors have to be considered to understand the full effect of converting from C to S status.

There are strategies for eliminating or minimizing some of these tax problems and for avoiding unnecessary pitfalls related to them. But a lot depends upon your company’s particular circumstances. Contact us to discuss the effect of these and other potential problems, along with possible strategies for dealing with them.

Selling mutual fund shares: What are the tax implications?

If you’re an investor in mutual funds or you’re interested in putting some money into them, you’re not alone. According to the Investment Company Institute, a survey found 58.7 million households owned mutual funds in mid-2020. But despite their popularity, the tax rules involved in selling mutual fund shares can be complex.

What are the basic tax rules?

Let’s say you sell appreciated mutual fund shares that you’ve owned for more than one year, the resulting profit will be a long-term capital gain. As such, the maximum federal income tax rate will be 20%, and you may also owe the 3.8% net investment income tax. However, most taxpayers will pay a tax rate of only 15%.

When a mutual fund investor sells shares, gain or loss is measured by the difference between the amount realized from the sale and the investor’s basis in the shares. One challenge is that certain mutual fund transactions are treated as sales even though they might not be thought of as such. Another problem may arise in determining your basis for shares sold.

When does a sale occur?

It’s obvious that a sale occurs when an investor redeems all shares in a mutual fund and receives the proceeds. Similarly, a sale occurs if an investor directs the fund to redeem the number of shares necessary for a specific dollar payout.

It’s less obvious that a sale occurs if you’re swapping funds within a fund family. For example, you surrender shares of an Income Fund for an equal value of shares of the same company’s Growth Fund. No money changes hands but this is considered a sale of the Income Fund shares.

Another example: Many mutual funds provide check-writing privileges to their investors. Although it may not seem like it, each time you write a check on your fund account, you’re making a sale of shares.

How do you determine the basis of shares?

If an investor sells all shares in a mutual fund in a single transaction, determining basis is relatively easy. Simply add the basis of all the shares (the amount of actual cash investments) including commissions or sales charges. Then, add distributions by the fund that were reinvested to acquire additional shares and subtract any distributions that represent a return of capital.

The calculation is more complex if you dispose of only part of your interest in the fund and the shares were acquired at different times for different prices. You can use one of several methods to identify the shares sold and determine your basis:

- First-in first-out. The basis of the earliest acquired shares is used as the basis for the shares sold. If the share price has been increasing over your ownership period, the older shares are likely to have a lower basis and result in more gain.

- Specific identification. At the time of sale, you specify the shares to sell. For example, “sell 100 of the 200 shares I purchased on April 1, 2018.” You must receive written confirmation of your request from the fund. This method may be used to lower the resulting tax bill by directing the sale of the shares with the highest basis.

- Average basis. The IRS permits you to use the average basis for shares that were acquired at various times and that were left on deposit with the fund or a custodian agent.

As you can see, mutual fund investing can result in complex tax situations. Contact us if you have questions. We can explain in greater detail how the rules apply to you.

AI for small to midsize businesses isn’t going away

Artificial intelligence (AI) has made great inroads into certain sectors of the U.S. economy. However, it hasn’t reached many small to midsize businesses (SMBs) in a major way … yet.

In 2021, AI analysis firm Unsupervised published a survey of 520 SMB owners that found 48% of them still found AI too cost prohibitive. Forty percent said their businesses lacked the staff expertise to use it. But the survey also found that one in five owners were implementing some form of AI, and 20% of respondents already using AI believed it had increased their profitability.

Defining the term

People sometimes confuse AI with data analytics or the application of intense mathematics. It’s so much more. AI generally refers to using computers to perform complex tasks typically thought to require human intelligence — for example, image perception, voice recognition, decision-making and problem solving.

Several types of technologies fall under the AI umbrella. One is machine learning, which applies statistical techniques to improve machines’ performance of a specific task over time with little or no programming or human intervention. Another is natural language processing, which uses algorithms to analyze unstructured human language in documents, emails, texts, conversation or otherwise. And a third is robotic process automation, which automates time-consuming repetitive manual tasks that don’t require decision-making.

Finding uses

Going back to the survey above, 28% of SMB owners said they were still determining precisely how to implement AI. The answer for your company depends on what you do and which technologies you rely on. Here are some examples of how businesses can use AI:

HR. AI software can significantly expedite the hiring process by soliciting and screening candidates. It can narrow the field and save interviewing time, freeing up HR staff to deal with other issues that require human attention. AI also might reduce the risk of discrimination claims because human subjectivity plays less of a role in the process.

Communications. Chatbots and other tools make it easier to maintain efficient and effective communications with customers and prospects. Specifically, these tools can respond to frequently asked customer service questions, allowing front-facing employees to focus on more targeted or complex issues.

Growing companies can also use AI tools to automate communications with vendors and employees. Doing so ensures the timely delivery of information and minimizes the chance of costly or embarrassing human errors.

Cybersecurity. Every company, no matter how big or small, faces the threat of hackers and ransomware schemes — and the risk has grown only more intense in recent months.

In fact, given the sheer number of cyberthreats out there, and the virtually infinite ways that cybercriminals can vary their attacks, AI is fast becoming an essential defensive tool. For example, through machine learning, AI can devise “classification algorithms” to detect spam and malware.

Proceeding with caution

AI for business — including SMBs — isn’t going away. Does this mean you should throw caution to the wind and spend exorbitantly on an AI solution today? Not at all. Like any technology initiative, an AI implementation project should involve careful research into your needs and a prudent budget. We can help you weigh the costs vs. benefits of any tech upgrades you’re considering.

Undertaking a pay equity audit at your business

Pay equity is both required by law and a sound business practice. However, providing equitable compensation to employees who perform the same or similar jobs, while accounting for differences in experience and tenure, isn’t easy. That’s why every company should at least consider undertaking a pay equity audit to assess its compensation philosophy and approach.

Legal background

The federal Equal Pay Act requires employers to provide men and women with equal pay for equal work in the same establishment. The jobs don’t need to be identical, but they should be “substantially equal.” Moreover, it’s not job titles, but job content — including skill, effort and responsibility — that determines whether jobs are substantially equal.

Many states have enacted their own equal pay laws, some of which are more stringent than the federal legislation. California, for example, requires employers to pay employees the same wage rates for “substantially similar work,” a larger umbrella than “same or similar jobs.”

Some other countries have also introduced laws around pay equity. The United Kingdom, for instance, requires some public companies to annually disclose the ratio of their chief executive officers’ pay to the lower, median and upper quartile of their employees’ pay.

In addition to helping to prevent legal woes, pay equity can offer bottom-line benefits. A company’s commitment to equitable pay can enhance its employer brand, boost employee morale and performance, and reduce the risk of negative publicity.

An involved process

The purpose of a pay equity audit is to:

- Uncover disparities in compensation,

- Identify the drivers behind them, and

- Develop ways to address the inequities.

Although the process can be quite involved, it’s typically worth the effort.

First, assemble participants from multiple departments — including HR, legal, and finance or accounting — to collect data on employee compensation, job classifications and demographics. This cross section of participants also will help ensure buy-in across the business.

The next step is determining how to group employees. That is, which ones will be considered to have substantially similar roles and, thus, should fall within the same pay range?

Some number crunching will come into play. For smaller employee groups, an analysis of, for example, differences in median pay between groups of employees might be enough to identify any unwarranted disparities. With larger groups, you may have to conduct more rigorous statistical analyses. For example, regression analysis can help control for variables, such as employees’ experience levels, when examining disparities.

Critical component

Over the past year, many workers have made it abundantly clear that they’ll leave a job if any of several employment components isn’t to their liking. Compensation is certainly one of these. Our firm can help support your efforts to conduct a pay equity audit.

It’s almost that time of year again! If you’re not ready, file for an extension

The clock is ticking down to the April 18 tax filing deadline. Sometimes, it’s not possible to gather your tax information and file by the due date. If you need more time, you should file for an extension on Form 4868.

An extension will give you until October 17 to file and allows you to avoid incurring “failure-to-file” penalties. However, it only provides extra time to file, not to pay. Whatever tax you estimate is owed must still be sent by April 18, or you’ll incur penalties — and as you’ll see below, they can be steep.

Failure to file vs. failure to pay

Separate penalties apply for failing to pay and failing to file. The failure-to-pay penalty runs at 0.5% for each month (or part of a month) the payment is late. For example, if payment is due April 18 and is made May 25, the penalty is 1% (0.5% times 2 months or partial months). The maximum penalty is 25%.

The failure-to-pay penalty is based on the amount shown as due on the return (less credits for amounts paid via withholding or estimated payments), even if the actual tax bill turns out to be higher. On the other hand, if the actual tax bill turns out to be lower, the penalty is based on the lower amount.

The failure-to-file penalty runs at the more severe rate of 5% per month (or partial month) of lateness to a maximum 25%. If you file for an extension on Form 4868, you’re not filing late unless you miss the extended due date. However, as mentioned earlier, a filing extension doesn’t apply to your responsibility for payment.

If the 0.5% failure-to-pay penalty and the failure-to-file penalty both apply, the failure-to-file penalty drops to 4.5% per month (or part) so the combined penalty is 5%. The maximum combined penalty for the first five months is 25%. Thereafter, the failure-to-pay penalty can continue at 0.5% per month for 45 more months (an additional 22.5%). Thus, the combined penalties can reach a total of 47.5% over time.

The failure-to-file penalty is also more severe because it’s based on the amount required to be shown on the return, and not just the amount shown as due. (Credit is given for amounts paid via withholding or estimated payments. If no amount is owed, there’s no penalty for late filing.) For example, if a return is filed three months late showing $5,000 owed (after payment credits), the combined penalties would be 15%, which equals $750. If the actual liability is later determined to be an additional $1,000, the failure-to-file penalty (4.5% × 3 = 13.5%) would also apply to this amount for an additional $135 in penalties.

A minimum failure-to-file penalty also applies if a return is filed more than 60 days late. This minimum penalty is the lesser of $435 (for returns due through 2022) or the amount of tax required to be shown on the return.

Reasonable cause

Both penalties may be excused by the IRS if lateness is due to “reasonable cause” such as death or serious illness in the immediate family.

Interest is assessed at a fluctuating rate announced by the government apart from and in addition to the above penalties. Furthermore, in particularly abusive situations involving a fraudulent failure to file, the late filing penalty can jump to 15% per month, with a 75% maximum.

Contact us if you have questions about IRS penalties or about filing Form 4868.

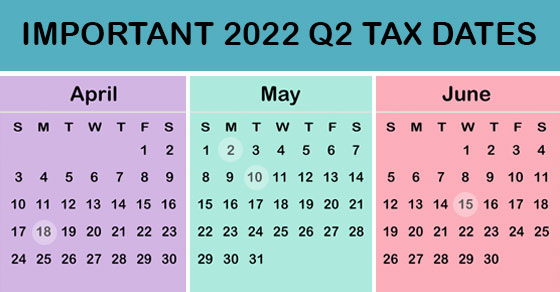

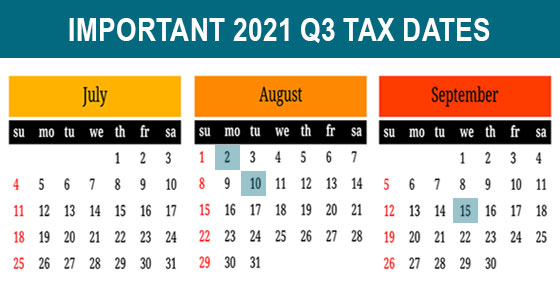

2022 Q2 tax calendar: Key deadlines for businesses and other employers

Here are some of the key tax-related deadlines that apply to businesses and other employers during the second quarter of 2022. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

April 18

- If you’re a calendar-year corporation, file a 2021 income tax return (Form 1120) or file for an automatic six-month extension (Form 7004) and pay any tax due.

- Corporations pay the first installment of 2022 estimated income taxes.

- For individuals, file a 2021 income tax return (Form 1040 or Form 1040-SR) or file for an automatic six-month extension (Form 4868) and paying any tax due. (See June 15 for an exception for certain taxpayers.)

- For individuals, pay the first installment of 2022 estimated taxes, if you don’t pay income tax through withholding (Form 1040-ES).

May 2

- Employers report income tax withholding and FICA taxes for the first quarter of 2022 (Form 941) and pay any tax due.

May 10

- Employers report income tax withholding and FICA taxes for the first quarter of 2022 (Form 941), if you deposited on time and fully paid all of the associated taxes due.

June 15

- Corporations pay the second installment of 2022 estimated income taxes.

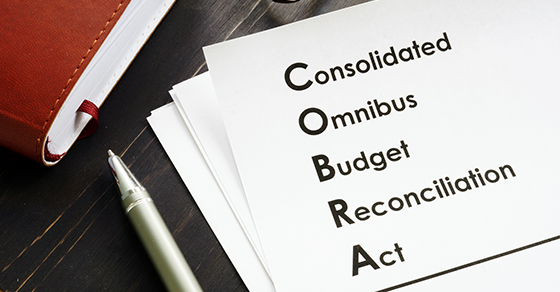

ERISA and EAPs: What’s the deal?

In recent years, more and more businesses have increased efforts to support the well-being of their employees. This means not only providing health care benefits, but also offering other initiatives designed to help workers cope with challenges such as substance dependence, financial planning, legal woes and mental health issues.

Among the options usually considered is an employee assistance program (EAP). These programs typically offer a set of benefits intended to address circumstances and challenges that might adversely affect employees’ ability to work. Benefits may include short-term mental health or substance abuse counseling or referral services, as well as financial counseling and legal services.

When considering an EAP, many business owners eventually ask a common question: Will the program be subject to the Employee Retirement Income Security Act (ERISA)?

Medical care

The answer depends on how the EAP is structured and what benefits it provides. Generally, an arrangement is an ERISA welfare benefit plan if it’s a plan, fund or program established or maintained by an employer to provide ERISA-listed benefits, which include medical services.

Indeed, the category of ERISA-listed benefits most likely to be provided by an EAP is medical care or benefits. Mental health counseling — whether for substance abuse, stress or other issues — is considered medical care. Accordingly, an EAP providing mental health counseling will probably be subject to ERISA. On the other hand, an EAP that provides only referrals and general information, and isn’t staffed by trained counselors, likely isn’t an ERISA plan.

Even if an EAP primarily uses referrals, it could still be considered to provide medical benefits if the individuals handling initial phone consultations and making the referrals are trained in an applicable field, such as psychology or social work. If the EAP provides any benefit subject to ERISA, then the entire EAP must comply with the law — even if it also provides non-ERISA benefits.

Beyond ERISA

When considering an EAP, you should first determine whether it will be subject to ERISA. The law’s provisions address critical compliance matters such as:

- Creating a plan document and Summary Plan Description,

- Performing fiduciary duties,

- Following claims procedures, and

- Filing IRS Form 5500.

However, an EAP that’s considered a group health plan will also be subject to the Consolidated Omnibus Budget Reconciliation Act (commonly known as “COBRA”) and certain other group health plan mandates, including mental health parity.

Another point to keep in mind: EAPs that receive medical information from participants — even if they only make referrals and don’t provide medical care — must comply with privacy and security rules under the Health Insurance Portability and Accountability Act (HIPAA).

An EAP might not be subject to other group health plan requirements. One that meets specified criteria can be defined as an “excepted benefit” not subject to HIPAA portability and certain Affordable Care Act requirements.

A worthy idea

The idea of offering your employees an EAP is well worth considering. This is particularly true now that businesses are under increased pressure to retain their workers. We can help you assess the costs, advantages and risks of one of these programs.

The tax rules of renting out a vacation property

Summer is just around the corner. If you’re fortunate enough to own a vacation home, you may wonder about the tax consequences of renting it out for part of the year.

The tax treatment depends on how many days it’s rented and your level of personal use. Personal use includes vacation use by your relatives (even if you charge them market rate rent) and use by nonrelatives if a market rate rent isn’t charged.

If you rent the property out for less than 15 days during the year, it’s not treated as “rental property” at all. In the right circumstances, this can produce significant tax benefits. Any rent you receive isn’t included in your income for tax purposes (no matter how substantial). On the other hand, you can only deduct property taxes and mortgage interest — no other operating costs and no depreciation. (Mortgage interest is deductible on your principal residence and one other home, subject to certain limits.)

If you rent the property out for more than 14 days, you must include the rent you receive in income. However, you can deduct part of your operating expenses and depreciation, subject to several rules. First, you must allocate your expenses between the personal use days and the rental days. For example, if the house is rented for 90 days and used personally for 30 days, then 75% of the use is rental (90 days out of 120 total days). You would allocate 75% of your maintenance, utilities, insurance, etc., costs to rental. You would allocate 75% of your depreciation allowance, interest, and taxes for the property to rental as well. The personal use portion of taxes is separately deductible. The personal use portion of interest on a second home is also deductible if the personal use exceeds the greater of 14 days or 10% of the rental days. However, depreciation on the personal use portion isn’t allowed.

If the rental income exceeds these allocable deductions, you report the rent and deductions to determine the amount of rental income to add to your other income. If the expenses exceed the income, you may be able to claim a rental loss. This depends on how many days you use the house personally.

Here’s the test: if you use it personally for more than the greater of 1) 14 days, or 2) 10% of the rental days, you’re using it “too much,” and you can’t claim your loss. In this case, you can still use your deductions to wipe out rental income, but you can’t go beyond that to create a loss. Any unused deductions are carried forward and may be usable in future years. If you’re limited to using deductions only up to the amount of rental income, you must use the deductions allocated to the rental portion in the following order: 1) interest and taxes, 2) operating costs, 3) depreciation.

If you “pass” the personal use test (i.e., you don’t use the property personally more than the greater of the figures listed above), you must still allocate your expenses between the personal and rental portions. In this case, however, if your rental deductions exceed rental income, you can claim the loss. (The loss is “passive,” however, and may be limited under the passive loss rules.)

As you can see, the rules are complex. Contact us if you have questions or would like to plan ahead to maximize deductions in your situation.

Taking the opposite approach: Ways your business can accelerate taxable income and defer deductions

Typically, businesses want to delay recognition of taxable income into future years and accelerate deductions into the current year. But when is it prudent to do the opposite? And why would you want to?

One reason might be tax law changes that raise tax rates. There have been discussions in Washington about raising the corporate federal income tax rate from its current flat 21%. Another reason may be because you expect your noncorporate pass-through entity business to pay taxes at higher rates in the future, because the pass-through income will be taxed on your personal return. There have also been discussions in Washington about raising individual federal income tax rates.

If you believe your business income could be subject to tax rate increases, you might want to accelerate income recognition into the current tax year to benefit from the current lower tax rates. At the same time, you may want to postpone deductions into a later tax year, when rates are higher, and when the deductions will do more tax-saving good.

To accelerate income

Consider these options if you want to accelerate revenue recognition into the current tax year:

- Sell appreciated assets that have capital gains in the current year, rather than waiting until a later year.

- Review the company’s list of depreciable assets to determine if any fully depreciated assets are in need of replacement. If fully depreciated assets are sold, taxable gains will be triggered in the year of sale.

- For installment sales of appreciated assets, elect out of installment sale treatment to recognize gain in the year of sale.

- Instead of using a tax-deferred like-kind Section 1031 exchange, sell real property in a taxable transaction.

- Consider converting your S corporation into a partnership or LLC treated as a partnership for tax purposes. That will trigger gains from the company’s appreciated assets because the conversion is treated as a taxable liquidation of the S corp. The partnership will have an increased tax basis in the assets.

- For a construction company, do you have long-term construction contracts previously exempt from the percentage-of-completion method of accounting for long-term contracts? Consider using the percentage-of-completion method to recognize income sooner as compared to the completed contract method, which defers recognition of income until the long-term construction is completed.

To defer deductions

Consider the following actions to postpone deductions into a higher-rate tax year, which will maximize their value:

- Delay purchasing capital equipment and fixed assets, which would give rise to depreciation deductions.

- Forego claiming big first-year Section 179 deductions or bonus depreciation deductions on new depreciable assets and instead depreciate the assets over a number of years.

- Determine whether professional fees and employee salaries associated with a long-term project could be capitalized, which would spread out the costs over time and push the related deductions forward into a higher rate tax year.

- Purchase bonds at a discount this year to increase interest income in future years.

- If allowed, put off inventory shrinkage or other write-downs until a year with a higher tax rate.

- Delay charitable contributions into a year with a higher tax rate.

- If allowed, delay accounts receivable charge-offs to a year with a higher rate.

- Delay payment of liabilities where the related deduction is based on when the amount is paid.

Contact us to discuss the best tax planning actions in light of your business’s unique tax situation.

360-degree feedback helps business owners see the big picture

Business owners are regularly urged to “see the big picture.” In many cases, this imperative applies to a pricing adjustment or some other strategic planning idea. However, seeing the big picture also matters when it comes to managing the performance of your staff.

Perhaps the best way to get a fully rounded perspective on how all your employees are performing is through a 360-degree feedback program. Under such an initiative, feedback is gathered from not only supervisors rating employees, but also from employees rating supervisors and employees rating each other. Sometimes even customers or vendors are asked to contribute.

Designing a survey

As you might have guessed, a critical element of a 360-degree feedback program is the written survey that you distribute to participants when gathering feedback. You can inadvertently sabotage the entire effort early on if this survey is poorly written or difficult to complete.

For starters, keep it as brief as possible. Generally, a participant should be able to fill out the survey in about 15 to 20 minutes. Ask concise questions that have a clear point. Be sure the language is unbiased; avoid words such as “excellent” or “always.” Ensure the questions and performance criteria are job-related and not personal in nature.

If using a rating scale, offer seven to 10 points that ask to what extent the person being rated exhibits a given behavior, rather than how often. It’s a good idea to use a dual-rating scale that includes both quantitative and qualitative performance questions.

Another good question is: To what extent should the person exhibit the behavior described, given his or her job role? By comparing the answers, you basically perform a gap analysis that helps interpret the results and reduces a rater’s bias to score consistently high or low.

Encouraging buy-in

To optimize the statistical validity of 360-degree feedback results, you need the largest sample size possible. Tell feedback providers how you’ll analyze their input, assuring them that their time will be well spent.

Also, emphasize the importance of being objective and avoiding invalid observations that might arise from their own prejudices. Ask providers to comment only on aspects of the subject employee’s performance that they’ve been able to observe.

Even with anonymous feedback, you should require some accountability. Incorporate a mechanism that would enable someone other than the subject of the evaluation — for instance, a senior HR manager — to address any abuse of the program. And, of course, ensure that subjects of the feedback process can work with their supervisors to act on the input they receive.

Taking it slowly

If a 360-degree feedback program sounds like something that could genuinely help your business, don’t rush into it. Discuss the idea with your leadership team and take the time to design a program with strong odds of success. Finally, bear in mind that you’ll likely have to fine-tune the program in years ahead to get the most useful data.

When inheriting money, be aware of “income in respect of a decedent” issues

Once a relatively obscure concept, “income in respect of a decedent” (IRD) may create a surprising tax bill for those who inherit certain types of property, such as IRAs or other retirement plans. Fortunately, there may be ways to minimize or even eliminate the IRD tax bite.

Basic rules

For the most part, property you inherit isn’t included in your income for tax purposes. Items that are IRD, however, do have to be included in your income, although you may also be entitled to an IRD deduction on account of them.

What’s IRD? It is income that the decedent (the person from whom you inherit the property) would have taken into income on his or her final income tax return except that death interceded. One common IRD item is the decedent’s last paycheck, received after death. It would have normally been included in the decedent’s income on the final income tax return. However, since the decedent’s tax year closed as of the date of death, it wasn’t included. As an item of IRD, it’s taxed as income to whomever does receive it (the estate or another individual). Not just the final paycheck, but any compensation-related benefits paid after death, such as accrued vacation pay or voluntary employer benefit payments, will be IRD to the recipient.

Other common IRD items include pension benefits and amounts in a decedent’s individual retirement accounts (IRAs) at death as well as a decedent’s share of partnership income up to the date of death. If you receive these IRD items, they’re included in your income.

The IRD deduction

Although IRD must be included in the income of the recipient, a deduction may come along with it. The deduction is allowed (as an itemized deduction) to lessen the “double tax” impact that’s caused by having the IRD items subject to the decedent’s estate tax as well as the recipient’s income tax.

To calculate the IRD deduction, the decedent’s executor may have to be contacted for information. The deduction is determined as follows:

- First, you must take the “net value” of all IRD items included in the decedent’s estate. The net value is the total value of the IRD items in the estate, reduced by any deductions in respect of the decedent. These are items which are the converse of IRD: items the decedent would have deducted on the final income tax return, but for death’s intervening.

- Next you determine how much of the federal estate tax was due to this net IRD by calculating what the estate tax bill would have been without it. Your deduction is then the percentage of the tax that your portion of the IRD items represents.

In the following example, the top estate tax rate of 40% is used. Example: At Tom’s death, $50,000 of IRD items were included in his gross estate, $10,000 of which were paid to Alex. There were also $3,000 of deductions in respect of a decedent, for a net value of $47,000. Had the estate been $47,000 less, the estate tax bill would have been $18,800 less. Alex will include in income the $10,000 of IRD received. If Alex itemizes deductions, Alex may also deduct $3,760, which is 20% (10,000/50,000) of $18,800.

We can help

If you inherit property that could be considered IRD, consult with us for assistance in managing the tax consequences.

Establish a tax-favored retirement plan

If your business doesn’t already have a retirement plan, now might be a good time to take the plunge. Current retirement plan rules allow for significant tax-deductible contributions.

For example, if you’re self-employed and set up a SEP-IRA, you can contribute up to 20% of your self-employment earnings, with a maximum contribution of $61,000 for 2022. If you’re employed by your own corporation, up to 25% of your salary can be contributed to your account, with a maximum contribution of $61,000. If you’re in the 32% federal income tax bracket, making a maximum contribution could cut what you owe Uncle Sam for 2022 by a whopping $19,520 (32% times $61,000).

More options

Other small business retirement plan options include:

- 401(k) plans, which can even be set up for just one person (also called solo 401(k)s),

- Defined benefit pension plans, and

- SIMPLE-IRAs.

Depending on your circumstances, these other types of plans may allow bigger deductible contributions.

Deadlines to establish and contribute

Thanks to a change made by the 2019 SECURE Act, tax-favored qualified employee retirement plans, except for SIMPLE-IRA plans, can now be adopted by the due date (including any extension) of the employer’s federal income tax return for the adoption year. The plan can then receive deductible employer contributions that are made by the due date (including any extension), and the employer can deduct those contributions on the return for the adoption year.

Important: The SECURE Act provision didn’t change the deadline to establish a SIMPLE-IRA plan. It remains October 1 of the year for which the plan is to take effect. Also, the SECURE Act change doesn’t override rules that require certain plan provisions to be in effect during the plan year, such as the provisions that cover employee elective deferral contributions (salary-reduction contributions) under a 401(k) plan. The plan must be in existence before such employee elective deferral contributions can be made.

For example, the deadline for the 2021 tax year for setting up a SEP-IRA for a sole proprietorship business that uses the calendar year for tax purposes is October 17, 2022, if you extend your 2021 tax return. The deadline for making the contribution for the 2021 tax year is also October 17, 2022. However, to make a SIMPLE-IRA contribution for the 2021 tax year, you must have set up the plan by October 1, 2021. So, it’s too late to set up a plan for last year.

While you can delay until next year establishing a tax-favored retirement plan for this year (except for a SIMPLE-IRA plan), why wait? Get it done this year as part of your tax planning and start saving for retirement. We can provide more information on small business retirement plan alternatives. Be aware that, if your business has employees, you may have to make contributions for them, too.

Business owners, lean into sales staff retention

Although there have been some positive signs for the U.S. economy thus far in 2022, many businesses are still reeling from last year’s “Great Resignation.” This trend of a historic number of workers voluntarily leaving their jobs, combined with the difficulty of hiring new employees, didn’t spare sales teams. However, one could say that the Great Resignation only threw gasoline on an existing fire.

Historically, sales departments have always trended toward higher turnover rates. Maybe you’ve grown accustomed to salespeople coming and going, and you believe there’s not much you can do about it. Or can you? By leaning into sales staff retention a little harder, you could avoid the worst of today’s uncomfortably tight job market and hang on to your top sellers.

Improve hiring and onboarding

Retention efforts shouldn’t begin with those already on the payroll; it should start during hiring and ramp up when onboarding. A rushed, confusing or cold approach to hiring can get things off on a bad foot. In such cases, new hires tend to enter the workplace cautiously or skeptically, with their eyes on the exit sign rather than the “upper floors” of a company.

Onboarding is also immensely important. Many salespeople can tell horror stories of being shown to a cubicle with nothing but a telephone on the desk and told to “Get to it.” Today, with so many people working remotely, a new sales hire might not even get that much attention. Welcome new employees warmly, provide ample training, and perhaps give them a mentor to help them get comfortable with your business and its culture.

Reward loyalty

Even when hiring and onboarding go well, most employees will still consider a competitor’s offer if the price is right. So, to improve your chances of retaining top sales producers and their customers, consider financial incentives.

Offering retention bonuses and rewards for maintaining and increasing sales — in addition to existing compensation plans — can help. Make such incentives easy to understand and clearly achievable. Although interim bonus programs might be expensive in the near term, they can stabilize sales and prevent sharp declines. When successful, a bonus program will help you generate more long-term revenue to offset the immediate costs.

Encourage ideas